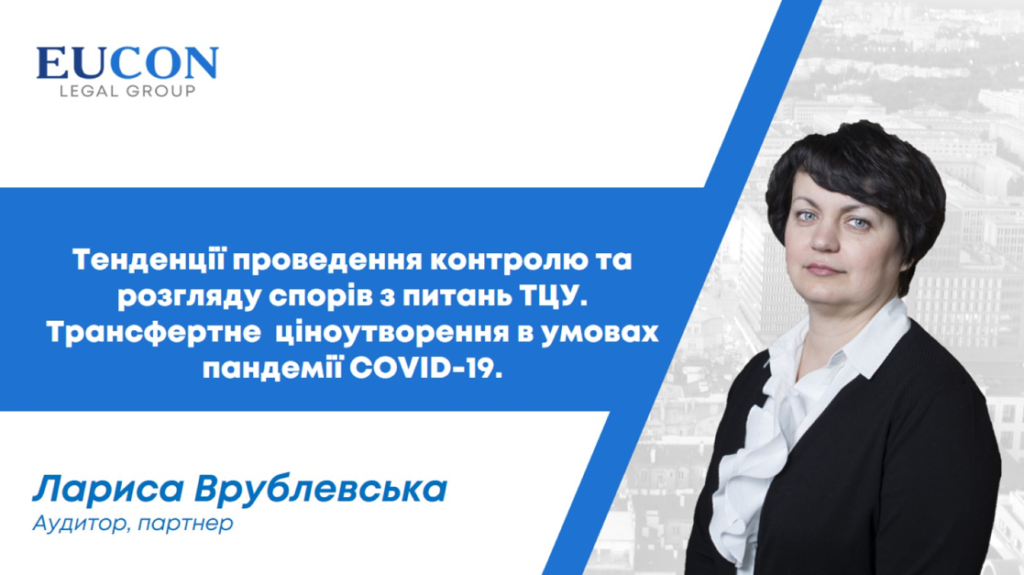

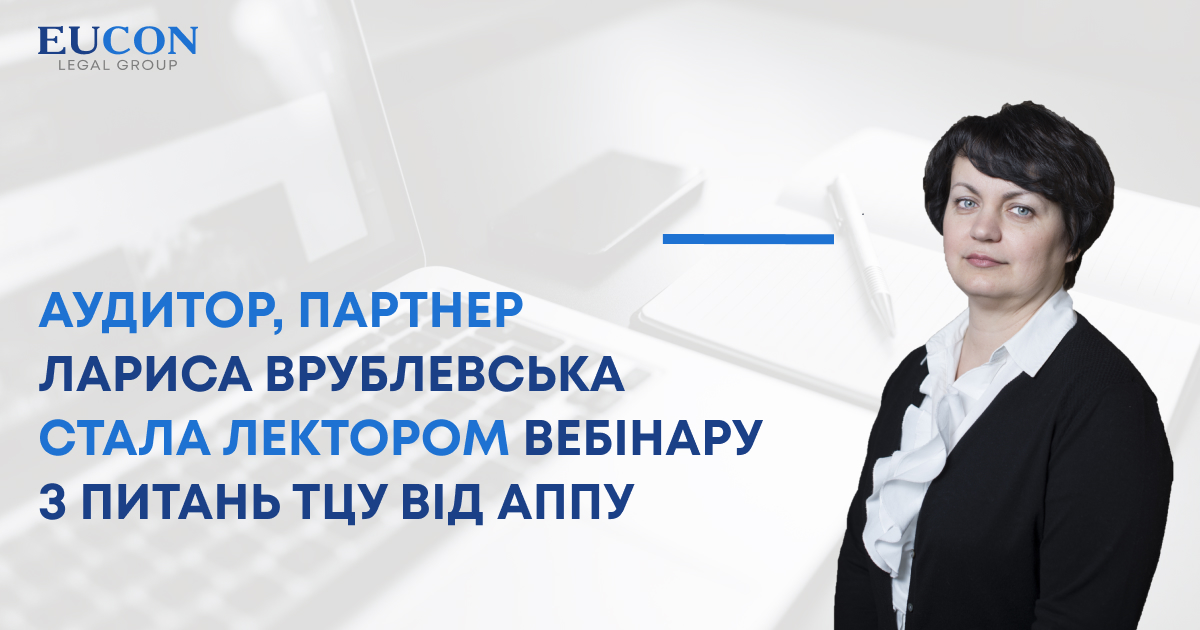

On June 15, another online webinar on transfer pricing was held by ATU. Larysa Vrublevska, once again an auditor, partner, and head of the TP practice of EUCON, became a speaker at the event of the Association of Taxpayers of Ukraine, speaking to the members of the organization with a lecture on the topic “Trends of control and consideration of disputes on TP issues. Transfer pricing in the context of the COVID-19 pandemic”.

Thus, the lecturer began the report with aspects of the impact of the COVID-19 pandemic, among which, in particular, the decrease in production/trade volumes, the general decrease in business profitability were named; change in business methods (online, refusal to maintain offices, warehouses, etc.); financial difficulties, dismissal of employees, reduction of budgets; restructuring of supply chains; exchange rate fluctuations, etc.

In the context of the impact of the current crisis, important problems in the field of transfer pricing were also discussed, including problems with the substantiation of losses, comparability analysis, fluctuations in the level of operating profit of negative exchange differences, the growth of certain types of unplanned costs, the impossibility of using historical/retrospective data, delay in receiving information on 2020 indicators, the impossibility of additional financing of losses by the main companies, redistribution of losses and costs within the Group, increased influence of additional risks (commercial, financial), etc.

Larysa Vrublevska voiced the recommended solutions that should be tried to solve the mentioned problems. For example, the expert advice trying a change of approaches regarding the use of data for comparative analysis, in particular, the application of OECD recommendations to tax administrations to ensure flexibility; change of TP methods; application of the profit sharing method, or several methods; try to prove the impact of force majeure circumstances; use the revision/cancellation of the terms of the existing ARA agreements/prior agreement on pricing; record in detail in the documentation from the TP all the circumstances that affect the results of activities, etc.

The lecturer also analyzed in detail the features of reporting in the field of TP for 2020, as well as methods of control in the field of transfer pricing – monitoring of controlled transactions, surveys on TP issues, conducting checks on compliance by the taxpayer with the principle of “an extended hand”.

The EUCON auditor did not ignore the issue of the moratorium on inspections, the assessment of fines, and the practical aspects of TP: 1) the criterion of the amount of revenue for the formation of the primary sample; 2) the quality of the final sample; 3) segmentation of account data; 4) choosing a period for analysis, using historical data.

The speech ended with a review and analysis of the current case law of the Supreme Court in the field of transfer pricing.